AMD's Momentum Builds as Intel Struggles: A Shifting Tech Landscape

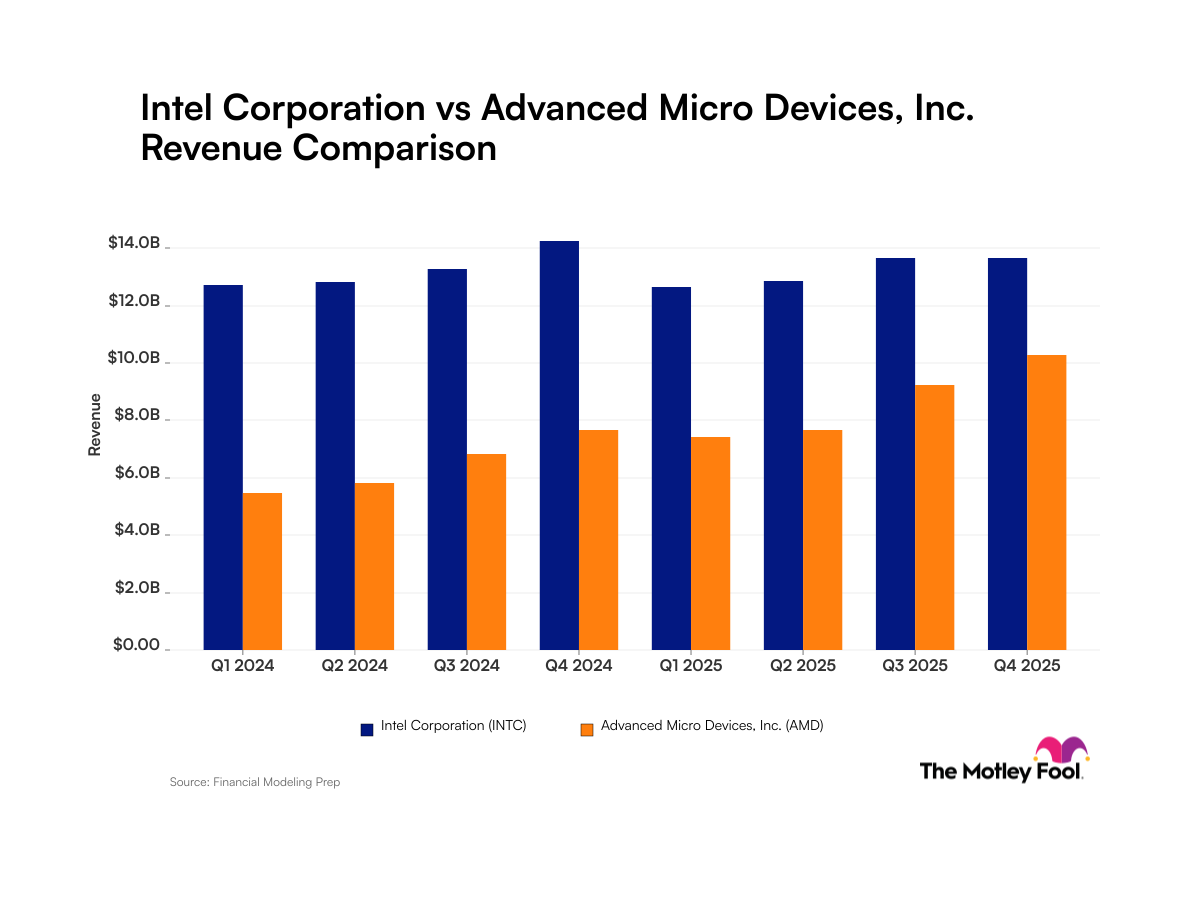

Advanced Micro Devices ($AMD) is fundamentally reshaping the semiconductor landscape, with revenue that has doubled over eight quarters while Intel ($INTC) faces mounting headwinds including stagnant growth and negative net income margins. The competitive dynamic between these two semiconductor giants has shifted dramatically, with AMD steadily gaining market share in critical CPU and data center GPU segments. Though Intel still holds a larger overall revenue base, the trajectory suggests a historic power shift in computing infrastructure—one that could see AMD surpass Intel in total revenue by 2027, particularly if its highly anticipated MI450 GPU launch gains traction in the booming artificial intelligence market.

Revenue Momentum and Profitability Divergence

The financial metrics paint a starkly different picture for the two chipmakers. AMD's revenue has expanded consistently, with eight consecutive quarters of strong growth that has doubled the company's top-line performance. This aggressive growth trajectory contrasts sharply with Intel's stalled growth, which has left the historic chip leader struggling to maintain momentum in its core markets.

More revealing than raw revenue figures, however, is the profitability story:

- AMD maintains a robust 16% net income margin, demonstrating operational efficiency and pricing power in competitive markets

- Intel faces a negative net income margin, indicating the company is losing money on operations despite its revenue scale

- AMD's consistent quarterly increases suggest sustainable, repeatable business model improvements

- Intel's profitability challenges reflect structural headwinds including manufacturing struggles, competitive losses, and elevated operational costs

This profitability divergence is particularly striking given that Intel remains the larger company by absolute revenue. Size, however, provides little comfort when a competitor is simultaneously growing faster and generating substantially higher profit margins. The mathematics of compounding growth suggest AMD could close—and potentially exceed—Intel's revenue lead within several years.

Market Share Gains in High-Growth Segments

The semiconductor industry's market dynamics have shifted decisively in AMD's favor, particularly in two critical segments:

CPU Market: AMD has made significant inroads in both server and consumer processor markets, displacing Intel from its long-held position of dominance. The company's EPYC server processors have captured meaningful data center share, while its Ryzen CPUs remain highly competitive in consumer segments.

Data Center GPUs: This segment has become increasingly valuable as artificial intelligence workloads proliferate across enterprise infrastructure. AMD's data center GPU offerings have positioned the company to capitalize on the AI infrastructure boom, a market where Intel historically held weak positioning.

These aren't peripheral markets. Data center and AI infrastructure represent some of the highest-margin, fastest-growing segments in semiconductor manufacturing. AMD's success in these areas explains why the company can maintain strong profitability growth even as it races to expand production capacity.

The MI450 GPU Wildcard

Perhaps most significant for AMD's growth outlook is the impending launch of the MI450 GPU, a next-generation accelerator chip designed for artificial intelligence and high-performance computing workloads. Industry analysts have projected that the MI450 could push AMD ahead of Intel in revenue by 2027—a timeline that underscores the transformative potential of AI-focused chip architecture.

The MI450 launch arrives at a critical inflection point in computing. Enterprise customers are investing massive capital in AI infrastructure, and GPU availability has become a bottleneck for many organizations implementing large language models and other advanced AI systems. A competitive, well-positioned AI GPU offering could capture substantial market share during this pivotal expansion phase.

Market Context: A Shifting Industry Landscape

These shifts reflect broader changes in the semiconductor industry:

Competitive Fragmentation: Intel's historical dominance has been challenged not just by AMD, but also by NVIDIA ($NVDA) in AI accelerators and emerging competitors in specialized chip categories. This fragmentation means Intel can no longer rely on cross-subsidization of weak business units with profits from dominant franchises.

Manufacturing Excellence: Intel's manufacturing challenges, including delays in advanced process node transitions, have contrasted unfavorably with AMD's foundry partnerships, which have enabled faster technology adoption without the capital burden of internal fab expansion.

AI Infrastructure Boom: The explosive growth in AI workloads has created entirely new market opportunities that Intel was poorly positioned to capture, while AMD has built competitive offerings with its data center GPU portfolio.

Customer Relationships: Customers increasingly view AMD as a credible alternative rather than a second choice, enabling the company to negotiate favorable pricing and secure priority allocation during supply-constrained periods.

Investor Implications: What This Means for Markets

For equity investors, this shift carries several critical implications:

Valuation Rerating: AMD's margin expansion and growth acceleration could justify continued multiple expansion, particularly if the company successfully executes its AI GPU strategy. Conversely, Intel's valuation compression reflects declining growth prospects and profitability challenges that may persist for multiple years.

Semiconductor Sector Dynamics: AMD's gains come directly from Intel's losses in many market segments, suggesting this represents market share shift rather than industry growth. Investors should carefully distinguish between companies benefiting from secular AI trends versus those merely capturing competitors' business.

Execution Risk: AMD's ability to deliver on the MI450 roadmap will substantially influence whether the company achieves the projected 2027 revenue-lead scenario. Manufacturing delays or competitive disappointments could significantly alter this timeline.

Diversification Benefits: Investors overweighting Intel in semiconductor sector allocations may want to reconsider positioning given the company's structural challenges, while AMD exposure offers more favorable growth dynamics, though at likely higher valuations.

Conclusion: A Historic Realignment Taking Shape

The competitive realignment between AMD and Intel reflects more than quarterly performance variation—it represents a fundamental shift in semiconductor industry leadership. AMD's doubled revenue over eight quarters, combined with superior profitability metrics and strategic positioning in high-growth AI infrastructure markets, suggests this trend has considerable momentum remaining.

While Intel retains advantages in certain legacy segments and still commands a larger revenue base, the trajectory strongly favors AMD. The company's MI450 GPU launch could prove transformative, potentially validating analyst projections that AMD will surpass Intel in total revenue within the next three years.

For the broader technology industry, this realignment matters profoundly. Intel has long served as a foundational computing infrastructure provider whose dominance enabled customers to standardize on Intel-based platforms. AMD's rise introduces competitive choice where near-monopoly once existed, ultimately benefiting customers through innovation and pricing pressure. Investors should watch this competitive dynamic closely—the outcome will shape semiconductor industry structure and computing infrastructure investment patterns for years to come.