Lead

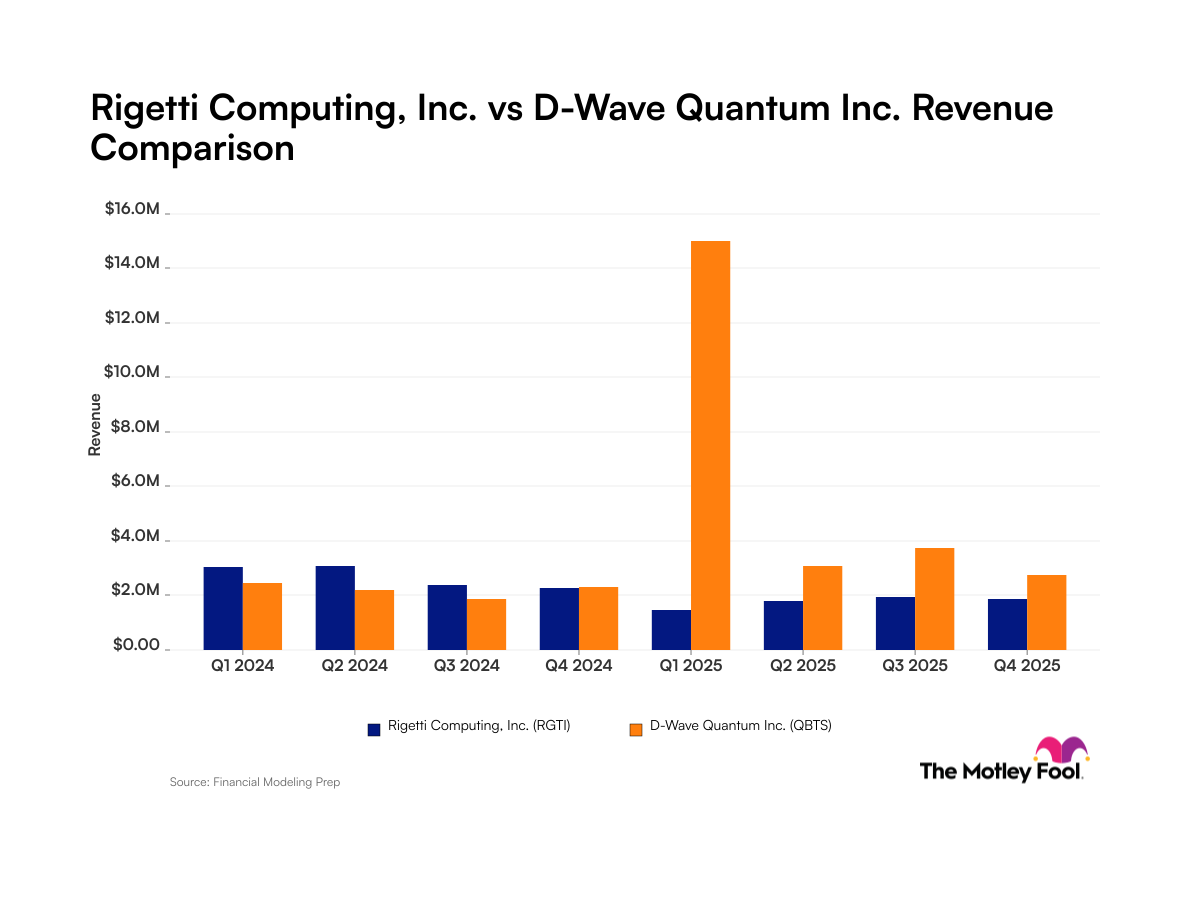

D-Wave Quantum and Rigetti Computing, two pioneering firms in the nascent quantum computing sector, are pursuing divergent commercial strategies as they race toward profitability and market dominance. While D-Wave generated $24 million in annual revenue, significantly outpacing Rigetti's $7 million, both companies remain deeply unprofitable and grapple with volatile quarterly performance that reflects the sector's inherent uncertainty. The contrasting revenue trajectories raise critical questions about which quantum computing approach will ultimately dominate the market and whether either company can establish sustainable, predictable growth patterns.

Key Financial Trajectories and Performance Metrics

D-Wave's stronger revenue position stems partly from a notable Q1 2025 spike, which elevated its annual figures relative to Rigetti's more modest performance. However, this revenue advantage masks deeper operational challenges confronting both organizations:

- D-Wave annual revenue: $24 million

- Rigetti annual revenue: $7 million

- Profitability status: Both companies operating at losses

- Revenue volatility: Significant quarterly fluctuations for both firms

- Q1 2025 performance: Notable spike for D-Wave driving year-end results

The disparity in revenue scales—D-Wave generating roughly 3.4x Rigetti's annual revenue—suggests different market traction, customer acquisition strategies, or product commercialization timelines. Yet neither organization has achieved positive net income, indicating that revenue growth has not translated into operational efficiency or sustainable business models. This gap between top-line growth and profitability remains the critical vulnerability for both quantum computing startups as they compete for limited venture capital and customer adoption.

The volatile nature of quarterly results for both companies underscores the unpredictable demand cycles in quantum computing. Unlike mature technology sectors with predictable procurement patterns, quantum computing adoption remains experimental and episodic, with enterprise customers conducting pilots rather than making large-scale deployments. This creates feast-or-famine revenue patterns that make financial forecasting exceptionally challenging and increase execution risk.

Market Context: Quantum Computing's Inflection Point

The quantum computing sector remains in its infancy, with commercial viability still largely theoretical despite decades of research investment. The industry faces several structural headwinds that affect both D-Wave and Rigetti:

Competitive Landscape: Both companies compete not only with each other but with well-capitalized technology giants—IBM, Google, and Amazon (through AWS)—that possess vastly larger R&D budgets and established customer relationships. IBM's quantum computing initiatives and Google's quantum supremacy claims represent formidable competitive threats, even as these tech giants pursue different technological approaches than D-Wave and Rigetti.

Technology Divergence: The quantum computing field encompasses multiple competing architectures and approaches. D-Wave has pioneered quantum annealing technology, focusing on optimization problems, while Rigetti pursues superconducting qubit systems suitable for broader quantum algorithm applications. This technological diversity prevents clear market winner predictions and creates uncertainty about which approach will ultimately prove most commercially viable.

Regulatory and Patent Environment: Quantum computing remains relatively unregulated, but intellectual property disputes and export controls surrounding quantum technology could significantly impact both companies' market access and competitive positioning. The nascent nature of quantum computing standards and lack of established industry benchmarks further complicate customer evaluation and purchasing decisions.

Customer Adoption Barriers: Despite growing interest from financial services, pharmaceuticals, and materials science sectors, quantum computers have not yet demonstrated clear economic advantages over classical computing for most real-world applications. This "quantum advantage gap" limits addressable markets and forces both companies to operate primarily in research and pilot program contexts rather than full production deployments.

Investor Implications and Risk Assessment

For investors evaluating quantum computing companies, these contrasting trajectories highlight critical strategic questions:

Scale and Sustainability: D-Wave's revenue lead suggests superior market positioning or product-market fit, but scaling revenue without achieving profitability raises concerns about unit economics and customer lifetime value. Investors must examine whether D-Wave's higher revenue reflects durable competitive advantages or simply earlier revenue recognition that won't sustain profitability improvements.

Path to Profitability: Neither company's current financial trajectory points toward near-term profitability. Operating losses imply ongoing capital requirements, increasing dilution risk for existing shareholders. The timeline to profitability—potentially 5-10 years given sector maturation rates—exceeds typical venture capital fund cycles, creating potential liquidity pressures.

Technology Risk: Quantum computing's technical challenges remain formidable. Quantum decoherence, error rates, and scalability issues continue to challenge both companies. Investors must assess whether management possesses realistic timelines for achieving commercially viable quantum advantage, or whether promotional narratives exceed engineering reality.

Market Concentration Risk: Both companies depend heavily on relatively small customer bases given their revenue scales. Losing major customers or facing delays in pilot programs could severely impact quarterly results, explaining observed volatility. Diversification into multiple customer verticals remains essential but difficult to achieve in niche markets.

Capital Efficiency: The revenue-to-loss ratio for both companies suggests significant capital inefficiency. Understanding burn rates, runway, and fundraising capabilities becomes essential for assessing bankruptcy or dilution risks. Companies requiring frequent capital raises face increasing valuation pressure and shareholder dilution.

Conclusion: Defining Success in Emerging Quantum Markets

The quantum computing sector stands at a critical inflection point where technical innovation must translate into demonstrable commercial value. D-Wave's revenue advantage over Rigetti reflects current market positioning but guarantees nothing about ultimate success or survivability. Both companies face the fundamental challenge of proving that quantum computing solves real problems better and more economically than classical alternatives—a threshold neither has definitively crossed.

Investors in quantum computing must distinguish between genuine technological progress and speculative hype. Metrics like revenue growth, while important, matter less than evidence of sustainable customer relationships, expanding addressable markets, and clear pathways to profitability. For both D-Wave and Rigetti, the next 18-24 months will prove decisive in determining whether they can transform experimental revenue into predictable, profitable operations or whether they'll face shareholder pressure to consolidate with larger technology incumbents. The quantum computing revolution remains probable; which private company will lead it remains genuinely uncertain.