Nvidia's AI Dominance Widens Revenue Gap Against Intel to Historic Proportions

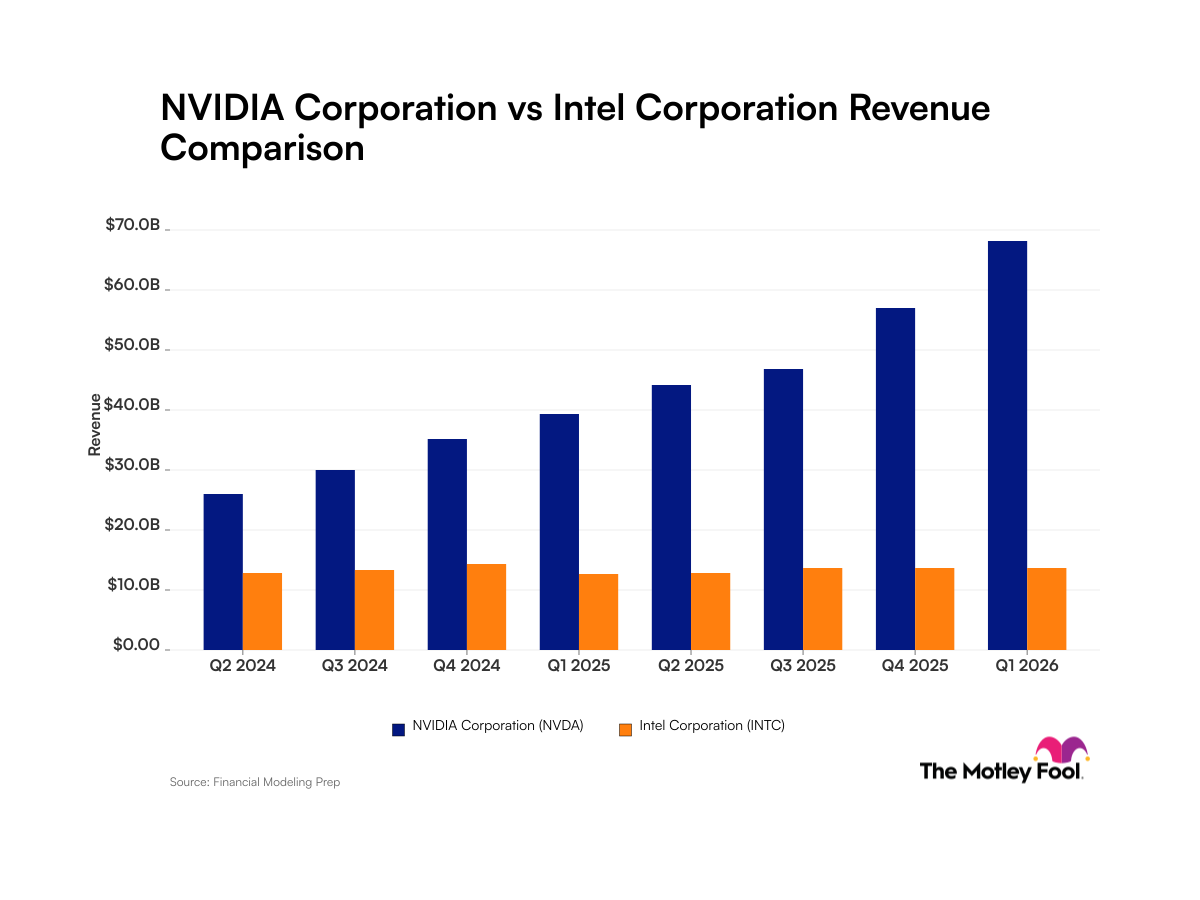

$NVDA has fundamentally reshaped the semiconductor hierarchy, posting eight consecutive quarters of rising revenue while establishing a commanding financial advantage over $INTC that reflects the seismic shift in computing toward artificial intelligence. Nvidia reported a 73% year-over-year revenue increase in its fourth quarter of 2024, translating to a trailing-12-month revenue of $188 billion—more than three times Intel's trailing revenue of $53 billion. While Intel demonstrated its own recovery momentum with a 7% year-over-year growth rate in Q1 2025—its strongest performance in eight quarters—the absolute gap between the two chip giants underscores a structural realignment in the semiconductor market driven by explosive demand for graphics processing units powering generative AI applications.

The Revenue Divergence: Scale and Momentum

The financial contrast between these two pillars of American semiconductor manufacturing tells a story of market disruption and strategic execution. Nvidia's consistent revenue acceleration, with eight consecutive quarters of growth, demonstrates sustained demand for its GPUs across data center infrastructure, cloud computing providers, and enterprise AI deployments. The 73% year-over-year growth rate in Q4 2024 signals that the AI boom remains in its growth phase, with no signs of demand saturation in sight.

Intel, conversely, has spent the past several quarters in stabilization mode. For an extended period, the chipmaker's revenue remained largely flat, reflecting competitive pressures and the delayed execution of its manufacturing roadmap. However, the 7% year-over-year growth reported in Q1 2025—described as the highest growth rate in eight quarters—suggests that Intel's strategic initiatives may be gaining traction. This includes:

- Recovery in data center chip demand

- Progress on next-generation process technology nodes

- Diversified product portfolio including CPUs for enterprise and consumer markets

- Potential wins in AI infrastructure segments

Despite this positive inflection, Intel's trailing-12-month revenue of $53 billion remains a fraction of Nvidia's $188 billion—a 255% differential that highlights the magnitude of Nvidia's market dominance.

Market Context: AI's Asymmetric Impact on Semiconductor Titans

The divergence between $NVDA and $INTC reflects broader industry dynamics that have fundamentally altered competitive positions within semiconductor manufacturing. Both companies are benefiting from the artificial intelligence boom, yet the benefits have accrued asymmetrically based on their respective product portfolios and market positioning.

Nvidia's dominance in GPU architecture has made it the de facto standard for AI workloads. Cloud providers including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform have rushed to procure Nvidia's GPUs—particularly the H100 and H200 series—to build out AI inference and training infrastructure. This demand has compressed lead times and supported robust pricing power, enabling Nvidia to expand profit margins while maintaining growth momentum. The company's software ecosystem, including CUDA, further entrenches its competitive moat by creating switching costs for developers and enterprises.

Intel has historically dominated the CPU market for data centers and personal computers, segments that have faced cyclical pressures and intense competition. While CPUs remain necessary components in AI infrastructure, they are complementary to GPUs rather than substitutes. Intel has attempted to compete in the discrete GPU market through its Arc GPU line and is developing AI accelerators, but these efforts remain in early adoption phases without the market penetration or software ecosystem maturity that Nvidia commands.

The regulatory and geopolitical environment also shapes competitive dynamics. Intel, as an American chipmaker, benefits from government incentives including the CHIPS and Science Act, which provides subsidies for domestic semiconductor manufacturing expansion. Nvidia, despite designing chips in California, outsources production to Taiwan Semiconductor Manufacturing Company (TSMC), creating different risk profiles related to geopolitical tensions over Taiwan. Both factors influence investor sentiment and long-term strategic positioning.

Profit Margins and Financial Health

Beyond raw revenue, the quality of earnings differs substantially between the two companies. Nvidia has expanded profit margins alongside revenue growth, reflecting:

- Premium pricing for specialized GPU architecture

- High gross margins on data center products (typically exceeding 60%)

- Operating leverage as revenue scales across fixed cost infrastructure

- Strong brand positioning that enables differentiation

Intel, by contrast, operates in a more commoditized segment of the semiconductor market. While data center CPUs command higher prices than consumer processors, competitive intensity from AMD and Arm-based processors has constrained margin expansion. Intel's manufacturing complexity and capital-intensive fabs add fixed cost burdens that limit profitability even during growth periods.

Investor Implications: Divergent Trajectories

For equity investors, the divergence between $NVDA and $INTC presents fundamentally different investment theses:

Nvidia investors are positioning for extended AI-driven growth, betting that semiconductor demand for artificial intelligence will continue expanding across data centers, autonomous vehicles, edge computing, and emerging applications. The company's ability to sustain margin expansion while growing revenues at 70%+ rates justifies premium valuation multiples relative to historical tech sector averages. Key investment risks include potential margin compression from competition (particularly from custom chips developed by cloud providers), China trade restrictions, and the possibility of AI capex cycles peaking.

Intel investors may view the company as undervalued based on improving operational metrics and government support for domestic manufacturing. The 7% year-over-year growth in Q1 2025 could mark the beginning of sustained recovery. However, investors must assess whether Intel can narrow the competitive gap with Nvidia and regain market share in high-margin segments. The company's capital expenditure program, supported by government grants, represents a long-term bet on manufacturing excellence and process technology leadership.

For the broader semiconductor sector, Nvidia's trajectory establishes a new threshold for scale and profitability. Competitors must achieve both revenue growth and margin expansion to justify valuations. Intel's recovery potential makes it a relative value play, appealing to investors skeptical of Nvidia's premium valuation or seeking exposure to semiconductor manufacturing consolidation.

Looking Ahead: Structural Dynamics and Market Evolution

The gap between Nvidia and Intel is unlikely to narrow significantly in the near term, barring major disruptions to AI demand or competitive breakthroughs. Nvidia's eight consecutive quarters of revenue growth, propelled by unabated demand for GPU compute capacity, suggest the company is capturing structural market share gains rather than benefiting from cyclical factors.

Intel's path forward depends on execution across multiple dimensions: advancing process technology to competitive parity, gaining traction in AI accelerator markets, and stabilizing margins in traditional CPU segments. The 7% growth rate in Q1 2025 is encouraging but insufficient to reverse years of relative underperformance. Success would require sustained double-digit growth sustained over multiple quarters—a challenging target given Intel's larger revenue base and competitive headwinds.

Ultimately, the Nvidia-Intel divergence reflects a semiconductor market in transition. AI has become the dominant demand driver, and companies positioned to supply the compute infrastructure for this shift have captured disproportionate value creation. Nvidia's $188 billion trailing revenue versus Intel's $53 billion is not merely a difference in scale—it represents a reshuffling of competitive advantage in an industry undergoing fundamental restructuring. For investors, tracking these divergent trajectories provides insight into how AI adoption translates into concrete financial performance and shareholder returns.