GoodRx Stalls While Hims & Hers Surges: Telehealth Divergence Widens

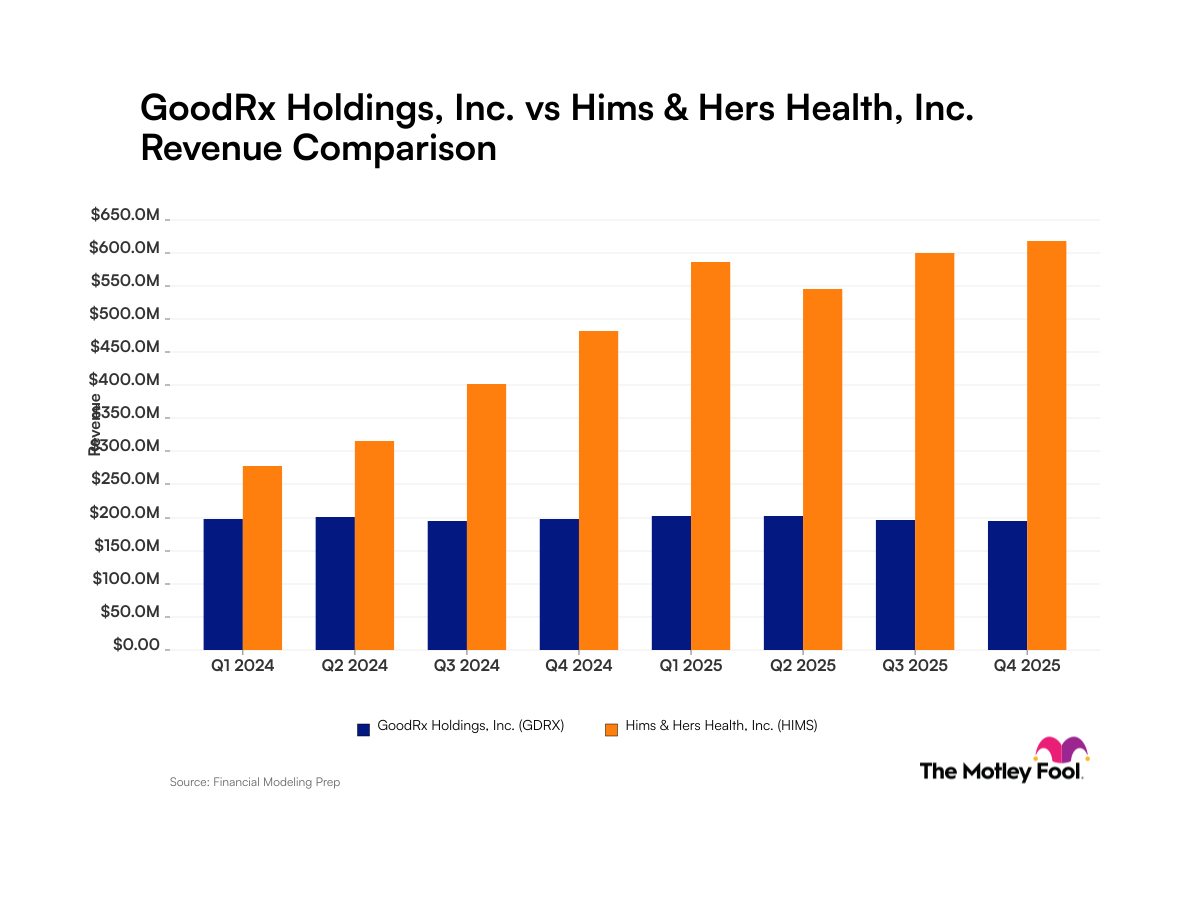

The digital healthcare landscape is revealing a stark competitive divide. While GoodRx grapples with revenue stagnation, posting a 4.4% year-over-year decline to $194 million in Q1 2026, rival Hims & Hers Health ($HIMS) is capitalizing on structural shifts in American healthcare with explosive 59% year-over-year revenue growth in Q4 2025. The divergence underscores a critical market reality: discount pharmacy platforms and telehealth providers are solving fundamentally different problems, and investors are increasingly rewarding the latter.

GoodRx's struggle arrives despite a bright spot within its operations. The company's Pharma Direct business surged 82% year-over-year, signaling that its wholesale pharmacy marketplace model retains strategic value. Yet this island of growth cannot offset declining performance in its core prescription discount platform, raising questions about whether the company's business model can sustain investor confidence amid changing healthcare dynamics.

The Tale of Two Digital Health Strategies

GoodRx built its empire on a straightforward premise: aggregate pharmacy pricing data and help consumers find the cheapest place to fill prescriptions. The company's $194 million in Q1 2026 revenue represents a contraction from the prior year period, suggesting that the discount pharmacy aggregation market may be maturing or facing headwinds from consolidation among major pharmacy chains and increased direct-to-consumer offerings from PBMs and pharmacy retailers.

The Pharma Direct business—which likely involves direct wholesale pharmaceutical distribution—demonstrated resilience with an 82% growth rate, indicating that GoodRx is successfully diversifying into higher-margin, business-to-business segments. However, the flagship consumer platform's decline suggests that this emerging business line has not yet scaled sufficiently to offset core revenue deterioration.

In sharp contrast, Hims & Hers Health is executing a textbook telehealth growth strategy. The company reported 13% subscriber growth in Q4 2025, expanding its user base while simultaneously growing revenue at 59% year-over-year. This combination—simultaneous user expansion and accelerating revenue—indicates that Hims is not only acquiring customers but also increasing monetization through upsells, expanded service offerings, or premium subscription tiers. The company's platform addresses a structural gap in American healthcare: insufficient access to primary care physicians and rising out-of-pocket healthcare costs that incentivize consumer self-direction.

Market Context: Why This Divergence Matters

The competitive positioning reflects broader market dynamics that transcend a simple earnings comparison:

-

Healthcare Cost Inflation: Americans face persistent healthcare cost pressures, with prescription drug prices remaining a significant burden. However, the real constraint is increasingly physician access rather than pharmacy pricing. Hims & Hers capitalizes on this shift by providing convenient, affordable telehealth consultations—services that GoodRx's platform does not offer.

-

Consolidation Among Pharmacy Chains: Major retailers like CVS, Walgreens, and Walmart have integrated healthcare services and negotiated directly with manufacturers, reducing the information asymmetry that GoodRx exploited during its growth phase. These chains now offer their own discount programs and digital tools, commoditizing the pure price-aggregation business.

-

Telehealth Legitimacy: Regulatory acceptance of telehealth has solidified since its pandemic-era surge. Insurance reimbursement parity and consumer adoption are now normalized, reducing execution risk for providers like Hims & Hers that deliver genuine medical services rather than comparative shopping.

-

Subscription Model Appeal: Hims & Hers' subscription-based revenue model provides recurring, predictable cash flows and higher customer lifetime value compared to GoodRx's transactional discount platform. The 13% subscriber growth in Q4 2025 demonstrates that consumers are willing to pay for convenience and ongoing access to healthcare providers.

GoodRx ($GDRX) faces a structural headwind: the market it pioneered is becoming less differentiated. Pharmacy benefit managers (PBMs), insurers, and retailers have incorporated price transparency into their own ecosystems, reducing the value of a standalone aggregation platform. While the Pharma Direct business shows promise, it represents a pivot away from GoodRx's core identity and may require significant capital investment and operational restructuring to scale meaningfully.

Investor Implications: Growth vs. Mature Market Dynamics

For equity investors and market strategists, this divergence carries multiple implications:

For $GDRX holders: The Q1 2026 revenue decline signals that core business momentum has stalled. The 82% growth in Pharma Direct is encouraging but insufficient to offset headline contraction. Investors should monitor whether management can articulate a credible path to returning the core business to growth or whether Pharma Direct becomes the primary focus of future capital allocation. The risk is that GoodRx becomes trapped between two markets—neither a leading pure-play discount platform nor a scaled telehealth provider.

For $HIMS investors: The 59% revenue growth with 13% subscriber expansion demonstrates that the company is executing on its core thesis: converting healthcare cost inflation and physician scarcity into customer demand for accessible, affordable telehealth. The combination of user growth and revenue acceleration suggests strong pricing power and/or successful cross-selling into the existing customer base. However, investors should remain alert to competitive pressures from both incumbent telehealth players and traditional healthcare providers expanding digital offerings.

Sector-wide implications: The broader digital health sector is maturing, and performance is increasingly bifurcated between providers offering genuine clinical services (like Hims & Hers) and transactional platforms (like GoodRx). The market appears to reward the former with higher multiples and stronger growth narratives. This trend suggests that investors should favor digital health companies with defensible clinical relationships, recurring revenue models, and network effects that create switching costs.

Regulatory considerations: Neither company faces imminent regulatory threats, but ongoing congressional scrutiny of PBM pricing practices could shift the competitive landscape. If PBM regulation limits their power to negotiate pharmacy prices, it could reintroduce value to price-aggregation platforms. Conversely, if telehealth continues to face favorable regulatory treatment, Hims & Hers will benefit.

Looking Ahead: Structural Shifts in Digital Healthcare

The divergence between GoodRx and Hims & Hers Health is not merely a quarterly earnings story; it reflects a fundamental transition in how consumers access and pay for healthcare. The primacy of price transparency—once GoodRx's competitive moat—has eroded as pricing information has become ubiquitous across pharmacy and insurance platforms. Meanwhile, the scarcity of physician time and the burden of healthcare costs have become the binding constraints for many consumers, creating sustained demand for telehealth solutions.

GoodRx's path forward likely requires accelerating the Pharma Direct transition and potentially exploring strategic partnerships or acquisition to gain telehealth capabilities. Without a significant shift in strategy, the company risks being overtaken by well-capitalized competitors in both the discount pharmacy and telehealth spaces.

Hims & Hers Health, by contrast, appears positioned to capture a meaningful share of America's primary care delivery, at least for routine consultations and common chronic conditions. The 59% growth rate demonstrates that unit economics remain favorable despite increasing competition. The critical question for the next 12-24 months is whether Hims can sustain growth while expanding margins—a challenge that will intensify as telehealth becomes mainstream and competitive pressures mount from both traditional healthcare providers and well-funded digital startups.