Palantir's AI Boom vs. BigBear's Stall: A Tale of Two Defense Tech Firms

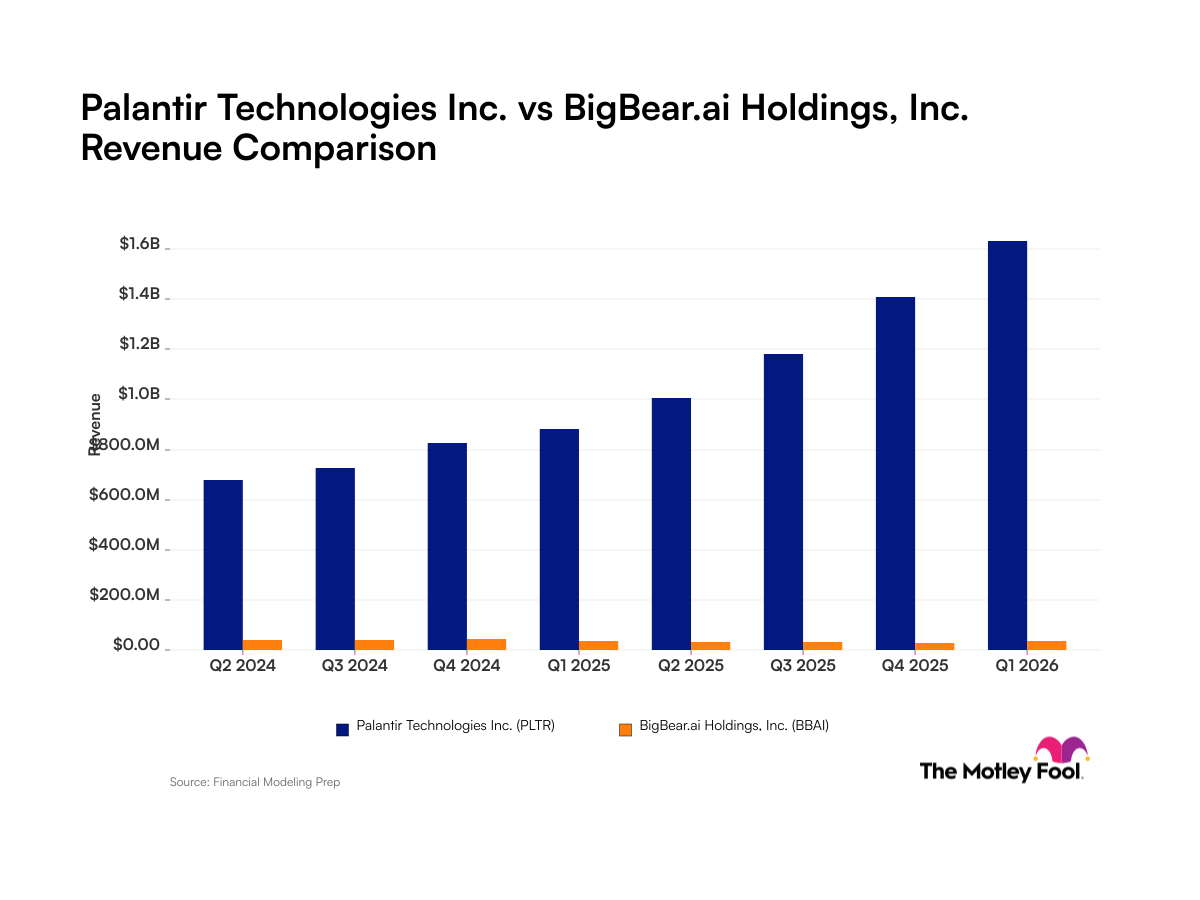

While both Palantir Technologies ($PLTR) and BigBear.ai operate in the booming artificial intelligence sector, their diverging financial trajectories paint starkly different pictures of success and struggle. Palantir has delivered eight consecutive quarters of revenue growth, capped by a towering $1.6 billion in Q1 2026 revenue with an impressive 85% year-over-year increase. By contrast, BigBear.ai reported Q1 2026 revenue of $34.4 million, representing a modest 1% year-over-year decline—a troubling sign for a company operating in one of the hottest technology markets. These contrasting narratives raise critical questions about execution, market positioning, and the widening competitive gap between established defense technology leaders and emerging AI specialists.

Key Details: Revenue Trajectories Tell the Story

Palantir's Consistent Ascent

The most striking aspect of Palantir's performance is its relentless consistency. Achieving eight straight quarters of quarter-over-quarter revenue growth represents exceptional operational discipline and market demand validation. The 85% year-over-year increase to $1.6 billion in Q1 2026 reflects more than just market enthusiasm—it demonstrates the company's ability to monetize its advanced data analytics and AI capabilities across multiple customer segments, particularly within government and defense contracting.

This growth trajectory suggests that Palantir has successfully positioned itself as the go-to platform for organizations requiring sophisticated data intelligence and AI-driven decision-making. The consistency of growth across eight consecutive quarters indicates that the company's revenue acceleration is not a one-time phenomenon but rather a sustainable business expansion reflecting genuine demand for its solutions.

BigBear.ai's Mounting Challenges

BigBear.ai's financial picture tells a starkly different story. With Q1 2026 revenue of $34.4 million, the company is roughly 46 times smaller than Palantir in absolute revenue terms. More concerning than the size differential is the 1% year-over-year decline, which signals stagnation despite operating in an AI market experiencing unprecedented growth.

This negative growth rate raises important questions about:

- Market penetration challenges

- Customer acquisition and retention difficulties

- Potential competitive pressures from larger players

- Execution issues relative to business potential

Market Context: The AI Defense Technology Landscape

Sector Momentum and Opportunity

The defense technology and AI markets are experiencing explosive growth. Government agencies worldwide are investing heavily in artificial intelligence capabilities for national security, intelligence analysis, and operational efficiency. This macro tailwind benefits companies operating in this space, which makes BigBear.ai's flat growth trajectory particularly noteworthy—the market is expanding, but the company is not capturing its proportional share of growth.

Competitive Positioning

The contrast between Palantir and BigBear.ai illustrates a critical dynamic in enterprise technology: scale and brand recognition compound over time. Palantir's established relationships with government agencies, proven track record in complex data integration projects, and widespread recognition as the "go-to" platform for intelligence analysis create significant competitive moats. The company's ability to deliver consistent double-digit growth suggests it is not only maintaining market share but expanding it.

BigBear.ai, by contrast, appears to be struggling to differentiate its offerings or achieve the same level of market penetration. Despite the company's focus on AI applications for national security, it has not translated sector growth into corporate revenue growth. This discrepancy suggests potential challenges in:

- Product-market fit relative to incumbent solutions

- Sales and marketing effectiveness

- Customer satisfaction and retention

- Competitive differentiation in a crowded marketplace

Regulatory and Market Environment

Both companies operate in a regulatory environment shaped by national security concerns and government procurement processes. However, established relationships and proven delivery track records—areas where Palantir has clear advantages—carry enormous weight in defense contracting. Government agencies tend to favor vendors with demonstrated capabilities and successful project histories, an advantage that becomes more pronounced as Palantir continues to grow and deepen customer relationships.

Investor Implications: What These Trends Mean

Growth Quality and Sustainability

For investors, Palantir's eight consecutive quarters of growth represents a significant credibility signal. Consistent quarter-over-quarter acceleration typically indicates:

- Strong underlying business fundamentals

- Robust demand from paying customers

- Effective sales and marketing execution

- Potential for margin expansion as scale increases

The 85% year-over-year increase is particularly noteworthy given that Palantir is already operating at a $1.6 billion annual run rate. Achieving this growth rate at significant scale is materially more challenging than growth in early-stage companies, making the consistency more impressive.

Red Flags and Concerns

BigBear.ai's stagnating revenue despite market tailwinds raises serious questions about investment merit. When a company cannot grow during a period of sector expansion, it often signals:

- Loss of competitive positioning to rivals

- Fundamental product or service inadequacy

- Management execution challenges

- Potential market saturation or saturation of addressable market

For equity holders, flat-to-declining revenue at a growth-stage company is particularly concerning, as it typically portends valuation compression and potential difficulty raising capital at favorable terms.

Market Share Implications

The divergence between Palantir and BigBear.ai suggests that Palantir is not merely benefiting from sector growth—it is gaining market share. In defense technology and AI contracting, market share concentration tends to increase over time as customers favor proven, large-scale vendors for mission-critical applications. Palantir's accelerating growth amid BigBear.ai's stagnation reinforces the likelihood that market share is consolidating toward the larger, more established player.

Valuation Considerations

For publicly traded investors, these divergent trajectories have significant implications for valuation. High-growth technology companies typically trade at premium multiples relative to stagnant peers. Palantir's sustained acceleration justifies higher multiples, while BigBear.ai's growth challenges may warrant multiple compression, all else equal. The market will likely reward consistent execution and penalize stagnation, creating a widening performance gap between the two companies.

Looking Forward: Widening Competitive Moats

The data suggests that the competitive gap between Palantir and BigBear.ai is likely to widen rather than narrow. Palantir's growing revenue base generates increased resources for R&D, customer support, and product development—capabilities that BigBear.ai may struggle to match at its current revenue level. Additionally, as Palantir deepens customer relationships and expands into new verticals, switching costs increase and competitive moats deepen.

For investors tracking these companies, the key takeaway is clear: consistent revenue growth in high-demand markets separates winners from losers over time. Palantir's eight consecutive quarters of growth, culminating in 85% year-over-year expansion, demonstrate a company capturing significant market opportunity with effective execution. BigBear.ai's inability to grow despite sector tailwinds suggests competitive challenges that may prove difficult to overcome without significant strategic changes. In the rapidly evolving AI and defense technology sectors, momentum matters—and Palantir has it in abundance.