Meta's AI Dominance Widens Gap With Snap as Ad Market Leaders Diverge

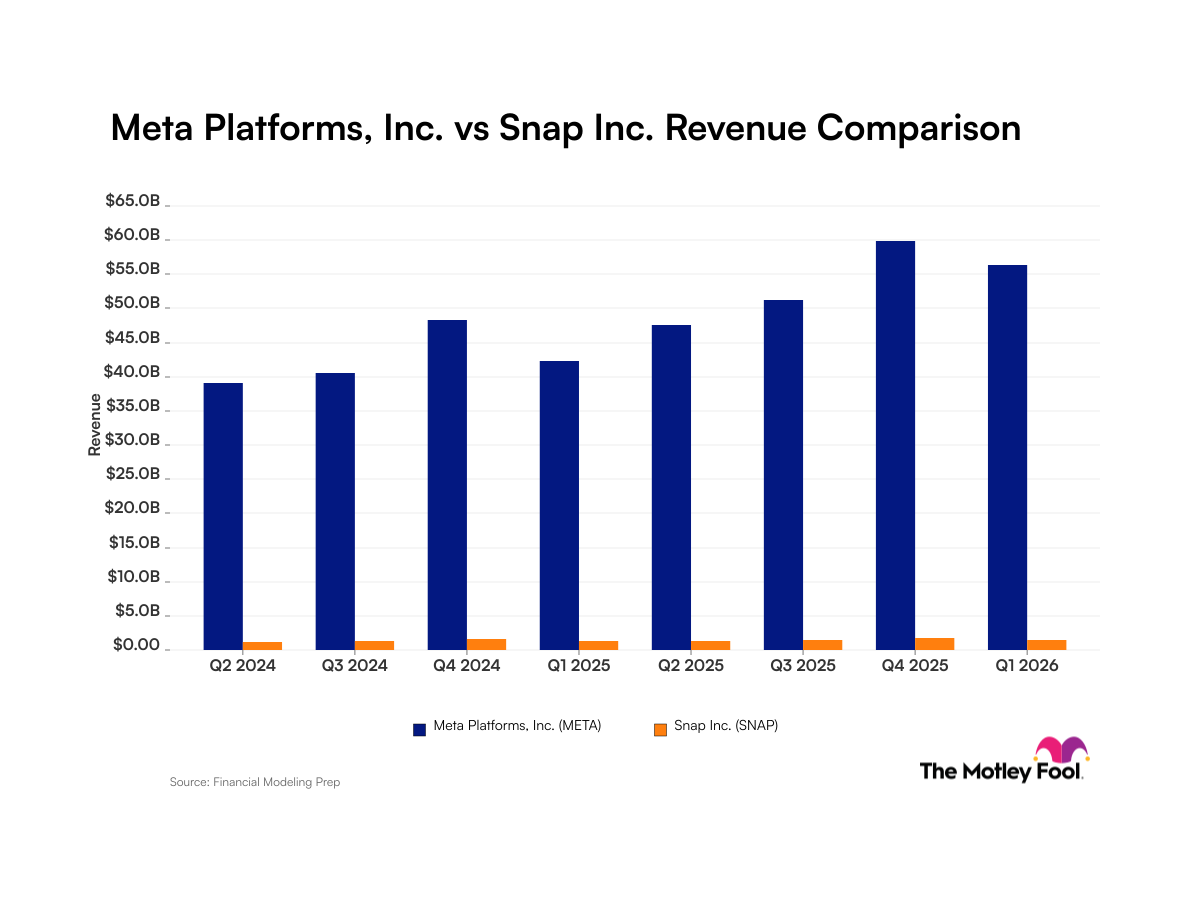

Meta Platforms and Snap are charting dramatically different courses through the social media advertising landscape, with first-quarter results exposing a widening gulf between the two competitors. While Meta delivered explosive 33% year-over-year revenue growth to reach $56.3 billion, Snap managed only a modest 12% increase to $1.5 billion—a performance gap that extends far beyond top-line metrics. The real story lies in profitability and strategic execution: Meta posted a commanding 48% net margin, while Snap remains unprofitable with a -6% net margin. For investors scrutinizing the social media advertising sector, these contrasting trajectories reveal fundamental differences in business models, technological investments, and competitive positioning.

The divergence raises critical questions about which company is better positioned to capitalize on the artificial intelligence revolution transforming digital advertising. Meta's superior scale, combined with aggressive AI investments in hardware and advertising infrastructure, stands in sharp contrast to Snap's struggle to achieve profitability despite its loyal user base and innovative augmented reality capabilities. Understanding what drives these differences is essential for investors evaluating exposure to the social media advertising sector.

Key Financial Performance Metrics

Meta's first-quarter results paint a picture of accelerating momentum across its sprawling ecosystem. The company's $56.3 billion quarterly revenue represents substantial growth that has exceeded analyst expectations, driven by:

- 33% year-over-year revenue growth significantly outpacing industry benchmarks

- 48% net profit margin demonstrating exceptional operational leverage

- Successful monetization of its core family of apps (Facebook, Instagram, WhatsApp)

- Growing contribution from its Reality Labs division, though still operating at losses

In contrast, Snap's first-quarter performance reflects the challenges facing smaller, more specialized platforms in the ad tech space:

- 12% year-over-year revenue growth, roughly one-third of Meta's expansion rate

- $1.5 billion in quarterly revenue, representing a tiny fraction of Meta's total

- -6% net margin indicating the company continues burning money on a net basis

- Heavy dependence on user growth and advertiser demand without achieving profitable scale

The profitability gap is perhaps the most striking difference. Meta's ability to generate 48 cents of profit for every dollar of revenue represents best-in-class performance for technology companies, while Snap's negative margins suggest fundamental challenges in its business model or cost structure. This disparity has profound implications for reinvestment capacity, shareholder returns, and strategic flexibility.

Market Context: The AI-Driven Divergence

These divergent financial trajectories reflect broader trends reshaping the digital advertising industry. Meta has aggressively positioned itself at the intersection of artificial intelligence and augmented reality, investing heavily in machine learning models that optimize ad targeting and placement. The company's AI-powered recommendation systems have become central to user engagement across Facebook and Instagram, driving superior ad relevance and pricing power.

Meta's hardware ambitions—particularly its Reality Labs division focused on metaverse infrastructure and augmented reality devices—represent a strategic bet on the future of computing and advertising. While currently unprofitable, these investments position Meta to potentially capture entirely new advertising categories as consumers increasingly interact with digital content through AR experiences. The company's willingness to absorb short-term losses in pursuit of long-term technological leadership distinguishes it from competitors constrained by near-term profitability requirements.

Snap, by contrast, has built a loyal user base around innovative camera and ephemeral messaging features. The platform's Stories format—initially dismissed by skeptics—has been widely copied and has become a standard feature across Meta's applications. However, Snap's smaller scale has created a challenging equation: the company must compete with Meta for advertising dollars while lacking the scale to achieve comparable profitability or reinvestment capacity.

The competitive landscape increasingly appears to favor larger, more diversified platforms with substantial AI capabilities. Meta's portfolio approach—spanning social networking, messaging, video, and emerging AR/VR technologies—provides multiple revenue streams and cross-selling opportunities that Snap's more focused model cannot replicate. This structural advantage manifests directly in the profitability gap and growth trajectories.

Regulatory pressures affecting both companies have been extensively documented, but Meta's scale provides greater resilience. While antitrust scrutiny and privacy regulations (particularly iOS privacy changes that impacted digital advertising) have affected both platforms, Meta's diversified revenue streams and absolute profitability cushion provide more strategic flexibility than Snap possesses.

Investor Implications: Which Platform Offers Better Value?

For equity investors evaluating exposure to the social media advertising sector, these Q1 results provide clear directional signals about competitive positioning and future cash generation capacity. Meta's 33% growth trajectory, combined with 48% net margins, generates substantial free cash flow that can fund ongoing AI investments, acquire emerging technologies, and potentially return capital to shareholders through dividends or buybacks. This combination of growth and profitability is rare in technology and historically has commanded premium valuations.

Snap's 12% growth rate, coupled with continued unprofitability, raises questions about the sustainability of its business model. The company must eventually achieve profitability through some combination of revenue acceleration and cost management. Until that inflection point arrives, Snap carries higher execution risk and limited financial flexibility to weather competitive pressures or macroeconomic headwinds.

Key investor considerations include:

- Growth sustainability: Meta's AI investments in ad optimization create competitive moats that should sustain above-market growth; Snap's growth may face compression as Meta continues expanding its AI capabilities

- Capital efficiency: Meta's profitability enables reinvestment in AI and hardware; Snap must first achieve breakeven before competing effectively on technology investments

- Margin expansion: Meta's 48% margins likely can expand further as AI-driven efficiencies compound; Snap's path to 20%+ margins remains unclear

- M&A and strategic optionality: Meta's financial fortress enables strategic acquisitions and pivots; Snap's balance sheet constraints limit optionality

Both companies operate in secular growth markets (digital advertising continues shifting online), but Meta appears better positioned to capture disproportionate share of that growth. The 33% versus 12% growth comparison reflects not merely market share gains but also the compounding effects of superior AI implementation and platform integration.

For value-conscious investors, Meta's superior margins and growth trajectory make it a more compelling investment thesis. Snap would appeal primarily to investors with high risk tolerance betting on a turnaround, new product success, or strategic asset sale.

Looking Forward: Momentum and Momentum Gaps

The Q1 results establish clear momentum divergence between Meta and Snap. Meta's combination of accelerating growth and exceptional profitability creates a virtuous cycle of reinvestment and competitive advantage that should persist through 2024 and beyond. The company's AI investments, while requiring substantial capital, appear to be generating measurable returns in advertising effectiveness and user engagement.

Snap faces the more challenging trajectory. The company must simultaneously accelerate growth (to justify its valuation) and improve profitability (to fund ongoing competitiveness). Achieving both simultaneously while competing against a far larger, more profitable, and increasingly AI-focused competitor creates an unenviable strategic position.

Investors should monitor whether Snap can demonstrate margin improvement in coming quarters—a prerequisite for restored investor confidence. Meta's investors, conversely, should focus on whether the company can convert its AI investments into sustained competitive advantages that justify continued premium valuations. The first-quarter results suggest Meta is executing on that strategy more effectively than competitive alternatives, making it the clear sector leader among major social media advertising platforms.