Joby's Revenue Lead Widens as Archer Scrambles in eVTOL Race

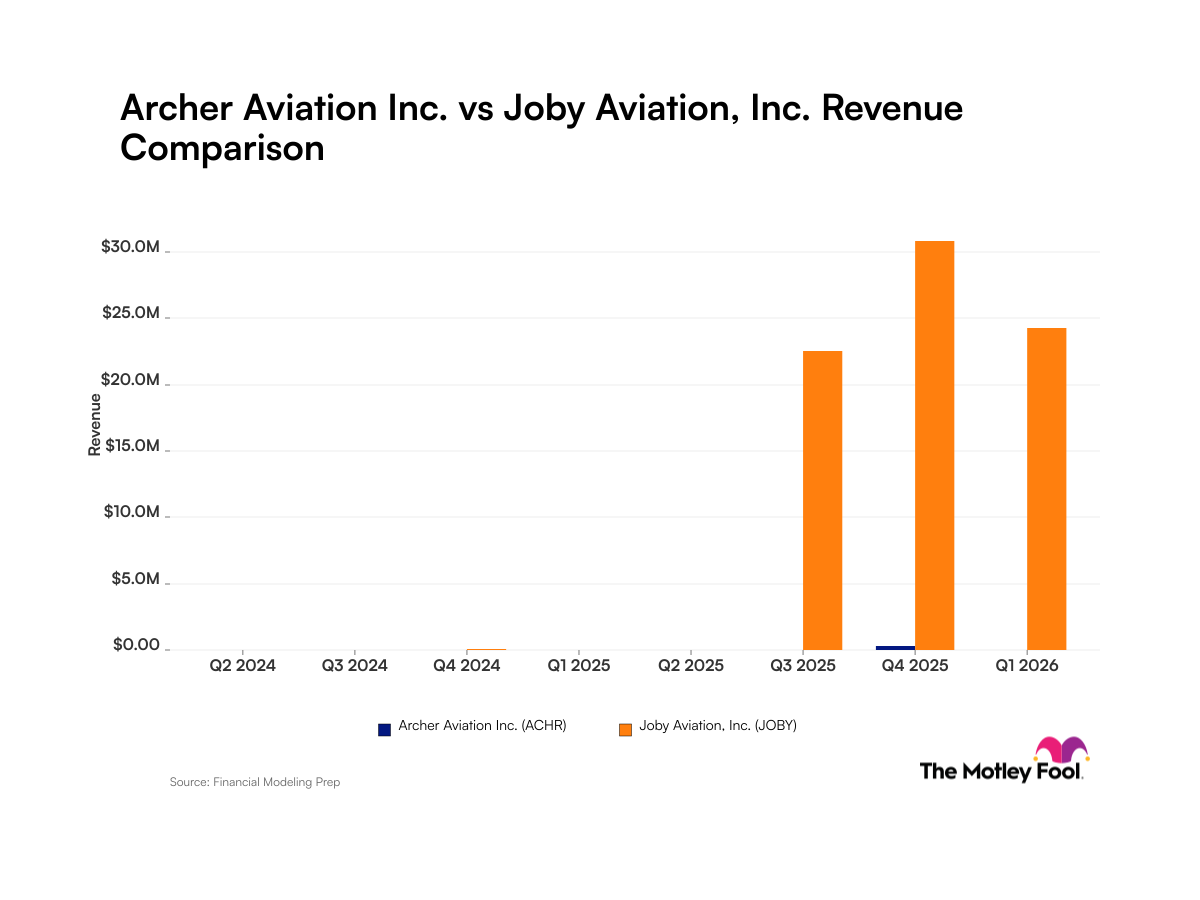

Joby Aviation has pulled decisively ahead of Archer Aviation in the race to establish commercial operations in the electric vertical takeoff and landing (eVTOL) market, with the former reporting $30.8 million in Q4 2025 revenue while its rival generated just $1.6 million in Q1 2026. The dramatic disparity reflects Joby's strategic acquisition of the Blade Urban Air Mobility platform, which instantly transformed the startup from a hardware manufacturer into an operator with established customer relationships and revenue streams. As both companies navigate the complex Federal Aviation Administration certification process in what analysts project could become a $1 trillion industry, Joby's early commercial traction has positioned it as the market leader—though industry observers caution that regulatory uncertainties and execution risks remain formidable obstacles for both competitors.

The Revenue Gap: Strategy and Timing Diverge

Joby Aviation's financial leap came courtesy of its transformative Blade acquisition, which brought an existing customer base and operational infrastructure into the fold. The $30.8 million quarterly revenue represents actual commercial operations rather than pilot programs or development contracts, marking a critical inflection point for an industry long dominated by technical demonstrations and investor presentations. This acquisition-driven approach allowed Joby to compress the typically lengthy path from hardware startup to revenue-generating operator, effectively leapfrogging the traditional validation timeline.

In contrast, Archer Aviation remains in the capital-intensive development and certification phase, with its $1.6 million in Q1 2026 revenue primarily stemming from milestone payments and limited operational activities. The company has been investing heavily in manufacturing facilities and regulatory compliance infrastructure, operating under the assumption that building robust certification credentials and production capacity would be essential foundations before scaling operations. Key metrics comparing the two companies reveal:

- Joby Aviation: $30.8M revenue (Q4 2025), Blade platform integration complete, operational flight services launched

- Archer Aviation: $1.6M revenue (Q1 2026), manufacturing setup phase, limited revenue-generating activities

- Combined addressable market: Estimated $1 trillion over industry maturation cycle

- Regulatory status: Both pursuing FAA Type Certification for commercial passenger operations

The strategic divergence between acquisition-led growth (Joby) and organic development (Archer) has produced dramatically different near-term financial profiles, though both companies remain years away from widespread commercial deployment.

Market Context: Certification and Competitive Dynamics

The electric vertical takeoff and landing sector occupies a unique position in aviation and transportation: it exists at the intersection of aerospace regulation, urban planning constraints, and technological possibility, yet commercial viability remains largely theoretical. The FAA certification process represents the single largest hurdle for both companies, requiring demonstrated safety records, technical specifications, manufacturing quality standards, and pilot training protocols across an entirely new aircraft category.

Joby's acquisition strategy effectively splits this problem into components: the Blade platform operates within existing regulatory frameworks for helicopter operations and air taxi services, providing immediate revenue while the company's proprietary eVTOL aircraft undergoes the longer FAA Type Certification process. This dual-track approach provides financial sustainability during the certification gauntlet—a critical advantage given that regulatory timelines remain unpredictable.

Archer Aviation has pursued a more traditional aerospace company trajectory, prioritizing manufacturing scale and certification readiness over near-term revenue, similar to the strategies employed by legacy aircraft manufacturers during development phases. This approach entails higher cash burn during pre-revenue stages but potentially positions the company as a more established manufacturer when commercial operations eventually commence.

The broader competitive landscape includes numerous global competitors pursuing similar objectives:

- Traditional aviation manufacturers (Airbus, Boeing, Textron) developing eVTOL platforms through acquisitions or internal programs

- Chinese competitors operating with fewer regulatory constraints in domestic markets

- Regional operators seeking hybrid solutions combining traditional helicopters with emerging technology

- Technology-first startups including Lilium, Volocopter, and others pursuing various design approaches

Joby's revenue lead provides more than just financial superiority—it offers operational validation, customer feedback, and a demonstrable business model that can attract institutional capital more readily than Archer's manufacturing-focused approach.

Investor Implications: Momentum, Uncertainty, and Long-Term Risk

For Joby Aviation shareholders, the Q4 2025 revenue achievement represents a fundamental inflection from venture-backed hardware development to legitimate commercial operations. This transition typically results in improved access to capital markets, enhanced valuation multiples, and reduced technical risk profiles in investor assessments. However, the revenue currently derives from Blade operations rather than Joby's proprietary eVTOL aircraft, raising questions about the durability of this advantage once Joby must demonstrate commercial viability of its own aircraft.

For Archer Aviation investors, the minimal Q1 2026 revenue highlights the capital intensity and extended timeline required for organic aerospace development. The company's path to profitability remains heavily dependent on:

- Successful FAA Type Certification timeline and scope

- Manufacturing scale-up efficiency and cost reduction

- Customer acquisition and demand validation post-certification

- Continued access to capital markets during pre-revenue scaling phase

Both companies face fundamental uncertainties that transcend current financial metrics:

Regulatory Risk: FAA certification timelines have proven difficult to predict. Delays would constrain revenue generation regardless of manufacturing readiness.

Capital Requirements: Scaling production, establishing service infrastructure, and managing certification compliance will require billions in additional capital. Market conditions and investor sentiment could rapidly shift.

Technology Validation: While both companies have demonstrated prototypes, commercial-scale operations at profitable unit economics remain unproven across the industry.

Market Demand: Initial pricing for eVTOL services ($5-$10 per mile) remains significantly higher than ground transportation, constraining addressable markets to premium segments (airport transfers, executive transport, emergency services).

Joby's revenue lead provides immediate advantages in valuation, capital access, and operational validation. However, the traditional aerospace industry has historically rewarded companies with proven manufacturing excellence, cost discipline, and long-term customer relationships—factors that Archer's deliberate approach may be cultivating. The $1 trillion addressable market could eventually support multiple competitors, but only those that achieve sustainable unit economics and regulatory approval.

Investors should monitor quarterly revenue growth rates, cash burn metrics, regulatory approval timelines, and aircraft unit cost trends as the primary indicators of competitive momentum. Joby's current lead appears decisive for near-term market positioning, but the industry's enormous scale and extended development timeline suggest that first-mover advantages may prove less durable than investors currently assume.

Both $JOBY and $ARCHER operate in an industry where technological disruption meets regulatory scrutiny, creating extraordinary potential rewards balanced against substantial execution risks. The coming 12-24 months—focused on certification milestones, manufacturing ramp, and demand validation—will substantially clarify which company's strategic approach proves optimal for capturing a portion of this transformative market.