Boeing's Make-or-Break Decision Looms

Boeing ($BA) stands at a critical inflection point that will largely determine its stock trajectory over the next decade. The aerospace giant must commit to developing a next-generation narrow-body aircraft to maintain competitive relevance in commercial aviation, a decision requiring approximately $50 billion in development capital. This unprecedented capital requirement arrives at a precarious moment for Boeing, which continues recovering from years of operational challenges and is not expected to generate sufficient free cash flow to self-fund the project until 2028 at the earliest. The strategic choices Boeing makes in the coming years—particularly regarding propulsion technology and financing mechanisms—will essentially define whether the company remains an industry leader or falls behind more agile competitors.

The narrow-body aircraft market represents the backbone of commercial aviation, accounting for the vast majority of passenger flights globally and generating consistent revenue streams for manufacturers. Boeing's current narrow-body offering, the 737 MAX, has regained market share following its return to service, but the aircraft is fundamentally an evolution of a platform that first flew in the 1960s. Meanwhile, Airbus ($EADSY) continues dominating the segment with the A320 family, and both manufacturers understand that the next generation of aircraft will need dramatically improved fuel efficiency, reduced operating costs, and lower emissions to meet increasingly stringent environmental regulations. The development timeline is equally critical—launching a new aircraft now would position it for service entry in the mid-2030s, aligning with market demand cycles and regulatory pressures.

The Engine Technology Dilemma

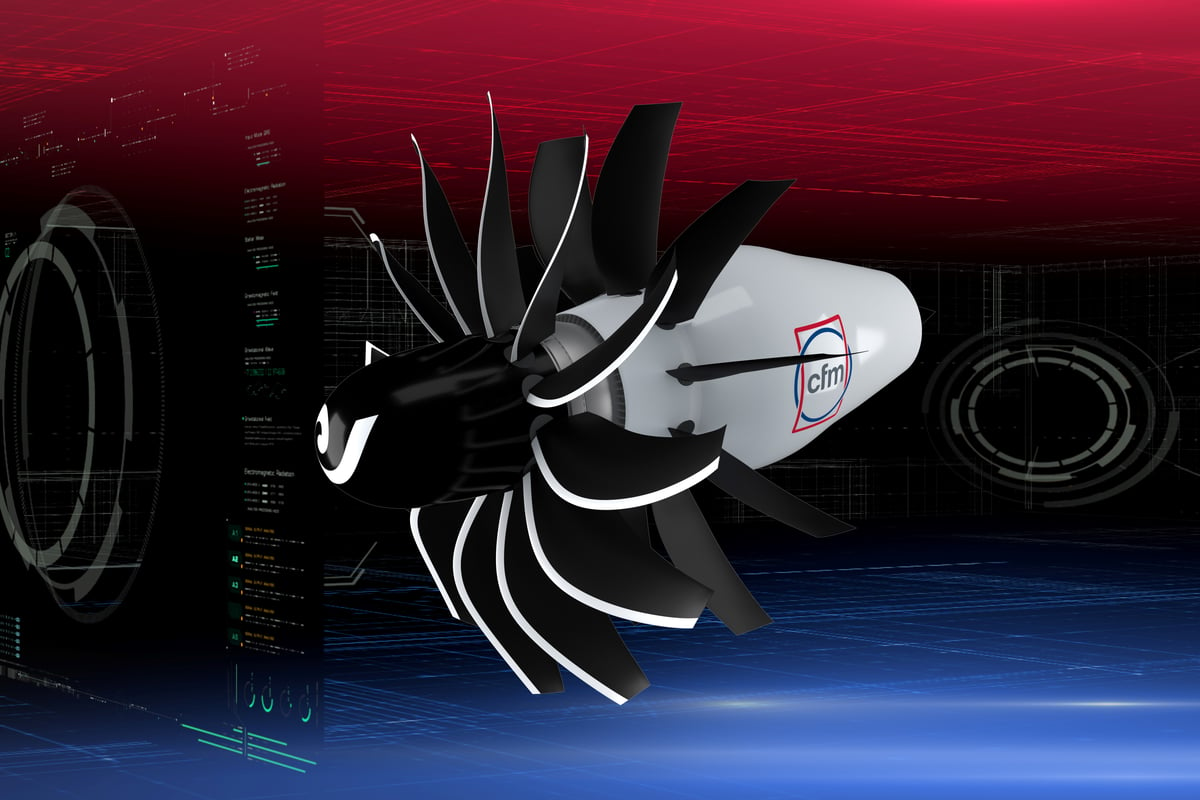

One of Boeing's most consequential decisions involves selecting between two distinct engine architectures, each with significant technical, financial, and competitive implications. The two primary options under consideration are ducted fan engines and open-fan engines (also called unducted fan engines). Open-fan engines, which have been developed by engine manufacturers like CFM International and Pratt & Whitney, promise superior fuel efficiency—potentially 20-25% better than current generation engines—making them highly attractive in an era of volatile fuel prices and carbon-conscious operators. However, open-fan engines present engineering challenges including noise levels, structural complexity, and manufacturing maturity concerns that remain unresolved at scale.

Ducted fan engines represent a more evolutionary approach, building on proven technology from existing platforms. These engines would deliver meaningful efficiency gains—though more modest than open-fan alternatives—while reducing technical risk and accelerating development timelines. The choice between these architectures will influence:

- Development costs and timelines: Open-fan engines could require 2-3 additional years of development

- Supplier relationships: Engine manufacturers have different capabilities and commitments to each technology

- Market positioning: Fuel efficiency gains directly translate to operating cost advantages for airlines

- Certification complexity: Open-fan engines may face more stringent regulatory scrutiny

- Competitive dynamics: Airbus's selection of similar technology would create standardization pressures

Airlines, Boeing's primary customers, have made clear their preference for maximum efficiency gains, creating pressure for the open-fan selection despite higher risk. However, Boeing's current financial constraints may necessitate the more conservative ducted-fan approach to manage both costs and execution risk.

Financing the Future: The Critical Challenge

The $50 billion funding requirement presents perhaps an even greater challenge than the technical decisions. Boeing cannot realistically self-finance a next-generation aircraft development program at current profitability levels. The company is not projected to generate more than $10 billion in annual free cash flow until 2028, and aircraft development programs typically span 8-10 years from launch to service entry. This means Boeing will need to deploy capital to fund the program while still maintaining competitive operations, paying down pandemic-era debt, and managing shareholder expectations.

Potential financing mechanisms under consideration likely include:

- Government support programs: The U.S. government has various mechanisms to support aerospace development

- Development partnerships: Risk-sharing arrangements with international suppliers or secondary manufacturers

- Export Credit Agencies: ECAs in the U.S. and allied nations often support major aerospace programs

- Hybrid financing structures: Combinations of debt, equity, and partnership models

- Stretched development timeline: Phasing development to align with cash flow improvement

The financing decision carries profound implications for shareholders. Aggressive external financing could dilute existing equity holders or increase debt burdens that constrain future flexibility. Conservative approaches might force Boeing to cede market share during critical development years. Unlike previous aircraft programs where Boeing maintained more operational strength, today's constrained financial position removes much of the company's traditional strategic flexibility.

Market Context and Competitive Pressure

Boeing's situation must be understood within the context of intense competition and evolving industry dynamics. Airbus has signaled its own commitment to next-generation narrow-body development, creating a zero-sum competitive dynamic where either company gaining first-mover advantage in efficiency gains could capture substantial market share for decades. Regional aircraft manufacturers and new entrants using composite materials and novel designs add additional competitive pressure.

Regulatory tailwinds also create urgency. International aviation bodies are implementing increasingly stringent emissions standards, and carbon-pricing mechanisms are making fuel efficiency a primary purchasing criterion for airlines. Aircraft entering service in the 2030s will compete on environmental metrics as much as economics, favoring the most advanced designs.

The commercial aviation market is also consolidating, with fewer major airline groups controlling increasingly larger shares of global capacity. These sophisticated operators demand advanced aircraft with demonstrable cost advantages and have significant negotiating leverage. Boeing must deliver generational improvements to justify the capital investment and convince airlines to commit to new platforms.

Investor Implications and Stock Outlook

For Boeing shareholders, the next decade's strategic decisions will likely prove more consequential than the past five years combined. The successful execution of a next-generation aircraft program would position the company for sustained profitability and cash generation from the 2030s forward, potentially supporting significant stock appreciation. Conversely, missteps in timing, technology selection, or financing could result in competitive disadvantage that takes decades to overcome.

Key variables investors should monitor include: announcements regarding engine technology selection, clarity on development timelines, details of financing mechanisms, progress on debt reduction, and evidence of operational cash flow improvement toward the $10 billion annual threshold. Any indication that Boeing is accelerating development timelines or pursuing external partnerships would represent bullish signals for long-term positioned investors.

The stock's performance will likely remain volatile through the decision period, as market participants price in different scenarios around timing and execution risk. However, investors with multi-year horizons should recognize that today's uncertainty represents the market attempting to price in outcomes across a wide spectrum of possibilities. A company that successfully navigates these decisions could deliver substantial returns; one that stumbles could face years of competitive disadvantage.

Looking Forward

Boeing's position in a decade will largely be determined by decisions made in the next 18-24 months. The company must balance technical ambition with financial reality, competitive pressure with execution capability, and long-term positioning with near-term stakeholder management. The $50 billion question isn't simply about whether Boeing can afford a new aircraft—it's about whether the company can afford not to develop one. For investors and industry observers, tracking Boeing's strategic choices will provide invaluable insight into whether the aerospace giant can reclaim its position as an innovation leader or will be forced into a defensive posture against more agile competitors. The stakes could hardly be higher.