Microsoft Outpaces Amazon in Growth Despite Revenue Gap

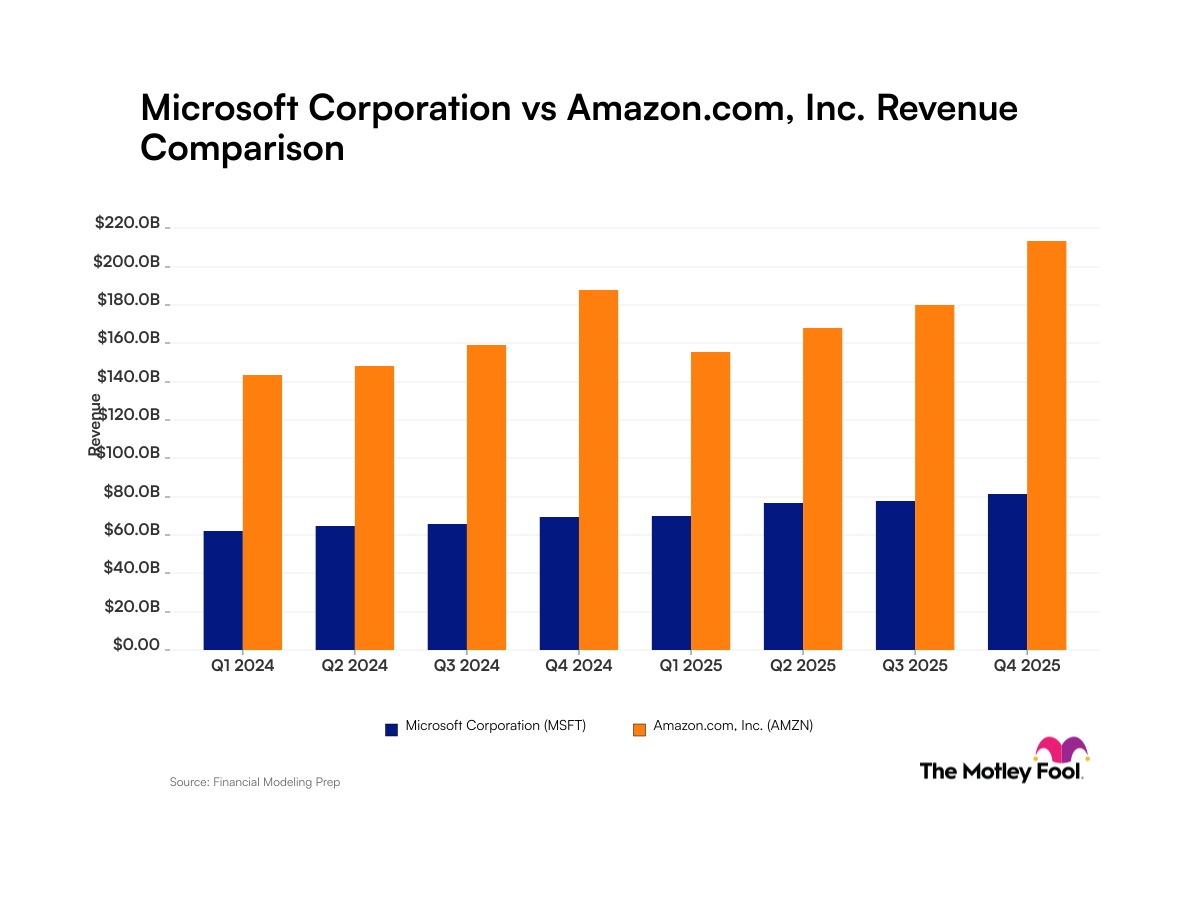

Microsoft and Amazon continue to dominate the technology sector, yet their diverging growth trajectories paint a compelling picture of shifting competitive dynamics. While Amazon maintains a substantial revenue advantage—generating nearly three times Microsoft's revenue—the Redmond giant is accelerating at a faster clip, posting a 17% year-over-year revenue increase in the December quarter compared to Amazon's 14%. This growth differential, though seemingly modest, signals a meaningful shift in momentum between the two tech behemoths and raises important questions about market leadership in the cloud computing era.

The performance gap becomes even more pronounced in cloud infrastructure, where Microsoft's Azure expanded 39% year-over-year, substantially outpacing Amazon Web Services (AWS) growth of 24%. This metric carries particular significance given that cloud computing has become the profit engine for both companies and a critical driver of investor valuations across the tech sector.

The Revenue Picture: Scale vs. Growth

On a raw revenue basis, Amazon maintains commanding market scale. The e-commerce and cloud giant's overall revenue footprint—nearly triple that of Microsoft—reflects decades of diversified business expansion across retail, logistics, advertising, and cloud services. However, Amazon's 14% quarterly growth rate, while respectable by absolute standards, lags the 17% expansion Microsoft achieved during the same period.

This growth rate divergence matters significantly for stock valuations. In the technology sector, where investors frequently apply premium multiples to companies demonstrating accelerating growth, a three-percentage-point spread can translate into meaningful differences in how Wall Street values these enterprises. For Microsoft ($MSFT), the faster growth trajectory provides narrative momentum, particularly as the company pivots toward artificial intelligence and enterprise cloud solutions. For Amazon ($AMZN), the slower growth rate—despite its market dominance—could invite investor scrutiny about maturation pressures and competitive encroachment.

The Cloud Computing Showdown: Azure's Remarkable Ascent

The cloud computing segment represents perhaps the most consequential competitive battleground between these two giants. Azure's 39% year-over-year growth significantly exceeds AWS's 24% expansion, marking a pronounced acceleration in Microsoft's cloud business relative to its incumbent rival.

AWS established cloud market dominance years ago, building what many viewed as an insurmountable lead through:

- Early market entry and infrastructure investment

- Comprehensive service breadth and ecosystem depth

- Entrenched enterprise customer relationships

- Consistent innovation and feature expansion

However, Microsoft's Azure has systematically narrowed this gap through several strategic advantages:

- Enterprise integration: Seamless integration with Microsoft's ubiquitous Windows, Office 365, and Dynamics 365 products creates native lock-in for existing enterprise customers

- Hybrid cloud positioning: Superior hybrid cloud capabilities bridging on-premises and cloud infrastructure

- AI integration: Aggressive incorporation of artificial intelligence capabilities, including the strategic OpenAI partnership, positioning Azure as the cloud platform of choice for AI workloads

- Competitive pricing and bundling: More aggressive pricing strategies and bundled licensing models that appeal to cost-conscious enterprises

The 39% versus 24% growth rate differential suggests Microsoft is successfully converting this strategic positioning into market gains, particularly among enterprises seeking to consolidate cloud vendors and leverage existing software investments.

Market Context: Industry Trends and Competitive Landscape

The competitive dynamics between Microsoft and Amazon must be contextualized within broader technology sector trends:

Cloud infrastructure consolidation: The cloud market shows increasing concentration around Microsoft Azure, Amazon AWS, and Google Cloud. The growth rate divergence suggests customers may be consolidating around Microsoft's tighter integration story rather than adopting multi-cloud strategies.

AI as a market differentiator: The integration of generative AI capabilities has become critical to cloud platform positioning. Microsoft's advantage through OpenAI partnership and Azure OpenAI Service offerings provides tangible competitive differentiation that AWS is working to match through expanded Bedrock offerings and other partnership strategies.

Enterprise software consolidation: Microsoft's existing relationships through Microsoft 365, Teams, Copilot, and business applications create natural expansion pathways into cloud infrastructure spending—a dynamic less available to Amazon, whose enterprise software footprint is comparatively limited.

AI services monetization: Both companies are aggressively monetizing AI capabilities. Microsoft's embedding of OpenAI features throughout its cloud and productivity suite provides multiple revenue streams. Amazon's broader infrastructure advantages position it well for training and inference workloads, though it may yield near-term cloud growth advantages to Microsoft in the enterprise segment.

Investor Implications: What This Means for Markets

For equity investors, these growth dynamics carry several important implications:

Valuation momentum: Microsoft's faster growth rate should support investor sentiment around the company's valuation multiples, potentially justifying premium pricing relative to Amazon. Growth-oriented investors may increasingly favor $MSFT over $AMZN on momentum grounds.

Cloud market share transitions: The growth rate divergence likely reflects actual market share gains for Azure relative to AWS. For Amazon shareholders, this represents a concerning structural shift in the company's highest-margin business segment. Management guidance in upcoming earnings calls will be critical—any acknowledgment of increased cloud competition could pressure Amazon's stock.

AI platform positioning: Microsoft's demonstrated ability to convert OpenAI partnership into cloud growth provides important validation that AI integration creates real business value. This could encourage Microsoft and discourage Amazon shareholders depending on how each company navigates the AI transition.

Broader tech sector implications: The Microsoft versus Amazon dynamic serves as a bellwether for how effectively technology incumbents can adapt to transformational shifts (cloud adoption, AI proliferation). Investors watching the broader tech sector will monitor this competition closely as evidence of which strategic approaches—Microsoft's integration focus versus Amazon's infrastructure breadth—win in the modern enterprise technology market.

Earnings quality considerations: Both companies demonstrate strong absolute growth, but the quality of this growth differs. Microsoft's growth benefits from high-margin cloud and productivity software revenues, while Amazon's overall growth is partially weighted by lower-margin retail operations. This distinction suggests Microsoft earnings growth may translate more directly into operating leverage and profitability expansion.

The diverging growth trajectories between Microsoft and Amazon, while both remain technology leaders, reflect a meaningful shift in competitive positioning. Microsoft's faster top-line expansion, particularly the pronounced Azure advantage in cloud computing, suggests the company's strategy of integrating AI capabilities and leveraging existing enterprise relationships is resonating with customers. For investors monitoring tech sector dynamics, this competition provides essential insight into how established technology incumbents compete during transformational periods and which strategic approaches create shareholder value in an increasingly cloud and AI-driven marketplace.